Portugal is an attractive destination for investors looking to diversify their real estate portfolio. With its strategic location, beautiful landscapes, and favorable investment climate, Portugal has become a popular destination for property investors. Here are five reasons why you should consider investing in Portuguese real estate with the help of GMG.

1. Golden Visa Program

Portugal's Golden Visa Program is one of the most popular residency-by-investment programs in Europe. The program allows non-EU citizens to obtain a residence permit in Portugal by investing in real estate. To qualify, you must invest a minimum of €500,000 in Portuguese real estate. GMG's team of experts can help you navigate the complexities of the Golden Visa Program and ensure a smooth application process.

2. Strong Rental Market

Portugal's rental market is strong, with high demand for properties in popular tourist destinations such as Lisbon, Porto, and the Algarve. Portugal's tourism industry has been growing steadily over the years, with a record number of visitors in recent years. This has created a high demand for short-term rentals, especially during the peak tourist season. GMG can help you find the best properties in the most desirable locations and manage your rental property to maximize your rental yield.

3. Affordable Property Prices

Compared to other European countries, Portugal offers relatively affordable property prices. You can find properties in popular destinations such as Lisbon and Porto at significantly lower prices than in other major European cities.

Lisbon: The average property price in Lisbon is around €4,454 per square meter, according to WithPortugal. Prices vary depending on the neighborhood, with the most expensive areas being Chiado, Principe Real, and Avenidas Novas.

Porto: The average property price in Porto is around €3,276 per square meter, according to WithPortugal. The most expensive areas in Porto are Foz do Douro, Boavista, and Cedofeita.

Compared to other major European cities, Lisbon and Porto offer relatively affordable property prices. For example, the average property price in London is around €14,680 per square meter, while the average property price in Paris is around €11,500 per square meter, according to data from Knight Frank, a global real estate consultancy firm.

Investors who are looking for good value for money can find affordable properties in Lisbon and Porto that offer high potential for capital appreciation and rental yield. With GMG's help, investors can access the best deals on properties that meet their investment criteria and maximize their return on investment. GMG can help investors find the best deals on properties that offer good value for money.

4. Low Taxes

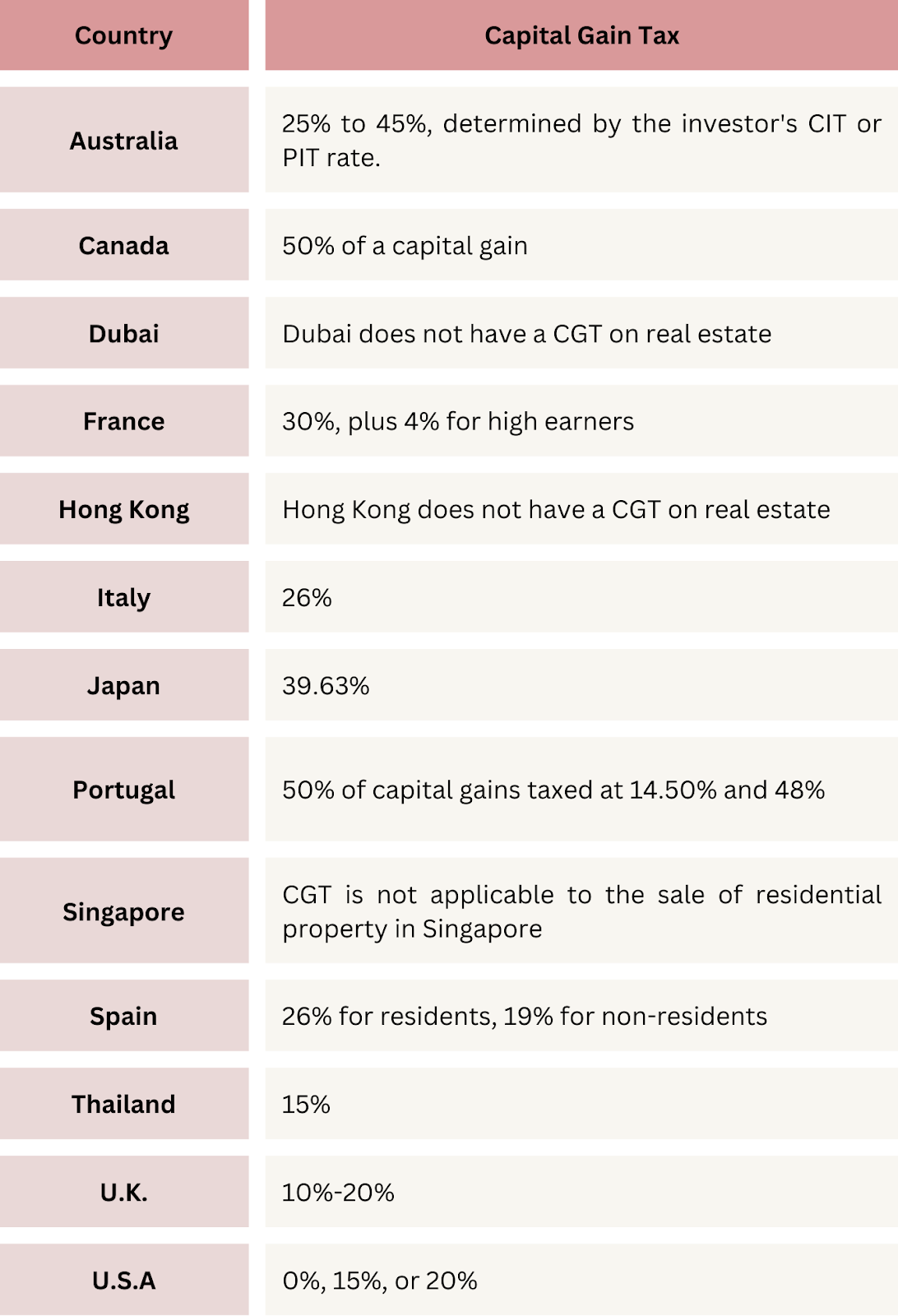

Portugal offers attractive tax incentives for property investors. The country has a flat tax rate of 28% on rental income, and capital gains tax is capped at 28%. Additionally, there is no inheritance tax or gift tax in Portugal, making it an attractive destination for wealthy investors looking to pass on their assets to their heirs. GMG can help you understand the tax implications of your investment and ensure compliance with Portuguese tax laws.

5. Mortgage financing for foreign nationals and U.S. expats

GMG can help foreign nationals and U.S. expats secure mortgage financing for Portuguese real estate investments. We have a team of mortgage specialists who can help you navigate the complexities of Portuguese mortgage financing and find the best mortgage products for your needs. We help investors understand the different mortgage options available and the required documentation for mortgage applications.

Investing in Portuguese real estate offers many benefits, from favorable tax incentives to high rental yields and good capital appreciation. Portugal's Golden Visa Program has made it an attractive destination for foreign investors looking to obtain residency in Europe. With its stable political climate and strong rental market, Portugal is a great option for those looking to diversify their real estate portfolio. GMG's team of experts can help you navigate the complexities of the Portuguese real estate market and ensure a successful investment. Connect with us today at hello@gmg.asia

Arabic

Arabic Chinese (Simplified)

Chinese (Simplified) English

English French

French German

German Korean

Korean Portuguese

Portuguese Spanish

Spanish Turkish

Turkish