Due to the sheer amount of investment opportunities, Dubai has become an attractive target for international investors. Expats looking to live and work in leading global business hubs that offer a luxurious quality of life and a good working environment have Dubai as a top option.

Here is what you need to know about investing in one of the fastest-developing countries in the world.

Amount of International Investors

With desirable tax-free policies and little to no limitations on profit expenses, Dubai has one of the most notable track records for acquiring overseas investors. According to Invest Dubai, the emirate’s efforts to streamline regulation, support innovation, and develop human capital have paved the way for its premier presence today as the preferred global FDI destination for both Fortune 500 companies and new entrepreneurs alike.

Consequently, Dubai has generated its highest amount of rental activity in decades, outpacing many western cities as the biggest investment destination with an average annual rental yield going upwards of five percent. Real estate blog Kaizen reports Dubai’s real estate sector to have attracted 19,757 foreign investors, of which concluded 24,666 investments worth over Dh35.6 billion.

Cost of Living

Due to its portrayal in the media, many assume you have to make a six-figure salary to even consider living in Dubai. However, the cost of living is not as high as one might think. In fact, one of the reasons Dubai is such a popular destination for foreign investors due to its lack of income tax and minimal sales taxes. Rental costs and living expenses are also quite low compared to other urban cities like London or New York. According to DMCC, the average rent for a studio apartment in the centre of Dubai is AED 5,141.89 (USD 1399,92), with monthly expenses of AED 3,477.89 (USD 946,88). Similarly, the average home price in the centre of Dubai is AED 2,791,502 (USD 760,000).

Visa Opportunities (Portugal, Spain, Dubai)

Recently, the UAE has relaxed restrictions on their coveted Golden Visa to attract more expatriates. Along with slimming down their minimum investment requirements from AED 5 million to AED 2 million, the UAE also doubled its validity from 5 years to 10 years. Under the new amendments, investors are now entitled to obtain long-term residence when purchasing property loans from local banks.

Top Areas in Dubai

According to 99acres, the most sought-after real estate properties in Dubai are within Dubai Hills Estate and Dubai Silicon Oasis, both of which are luxurious residential areas. Palm Jumeirah, Dubai Marina, and Dubai Downtown are also popular locations because of their exclusivity and glamor.

The listings in these areas suggest that residential apartments dominate almost 75% of the housing demand in Dubai. Among them, one-bedroom and two-bedroom units have the highest demand, with prices starting from around AED 66,700.

Another popular configuration in Dubai is independent houses that generally comprise two bedrooms and above. The prices of these standalone units begin at AED 111,160.

GMG Dubai Mortgage

With up to 25 years, maximum 75% loan-to-value, and interest rates starting from 5%, foreign investors and non-Dubai residents can now obtain attractive terms to finance their Dubai property purchase.

GMG designed this program specifically for foreign nationals with particular focus on the ease of qualifying. The speed of the entire loan process will surprise you.

Get in touch with us today to find out more at hello@gmg.asia.

The "Bizarro World" references Bizarro Superman, a supervillain who lives in a world where everything is opposite. Here's a great explanation from the TV show Seinfeld.

This reminds me of the world we live in now; mortgage rates double in 10 months, and yet, rental yields continue to increase double digits, year-on-year.

I have been telling our clients over the past few months that it is a great time to be owning a home in the U.S. for investment income. Most of us have lived through a few economic cycles, and for most of my career, 30-year fixed rates were between 6-7%, which is when I got my first mortgage in 2006, similar to where rates are now.

However, back then, you owned homes almost as leveraged equity, not like what it's meant to be, more similar to a bond.

When academics say real estate is an inflation hedge, that is a peculiar concept since we have not really seen any inflation since the 70s, so not many of us know what that means in real life.

Till now….

This world is very different. Good or Bad, the fact is that there are significantly more people who need housing, millennials are unable to afford homes, and the rising rates have squeezed out the marginal buyer, and all of the above need to live somewhere.

My colleagues hear me say this ad nauseam,

"We will be in a world where 30-year fixed-rate mortgages are 7%, but rental yields are 10-15% very soon".

I will try to explain why in this report.

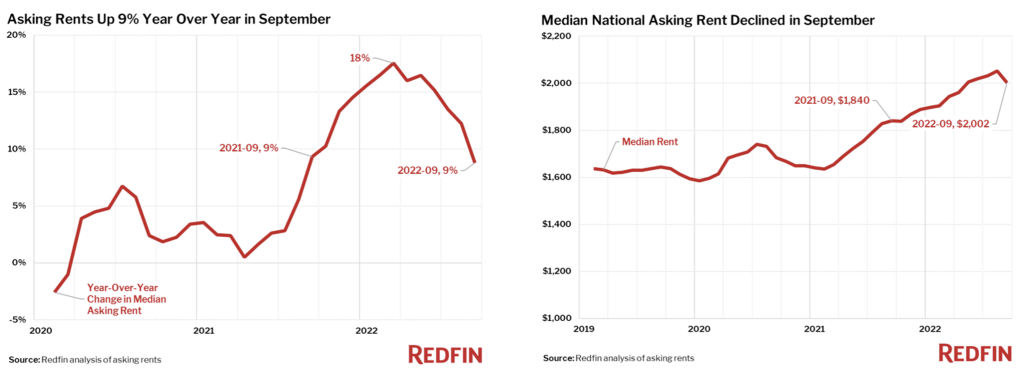

A few days ago, on October 13th, Redfin reported that the Median U.S. Asking Rent rose 9% year-over-year in September to $2,002, the slowest growth since August 2021 and the first single-digit increase in a year. Sure the article makes it sound bearish.

Wait a minute? (sound of car screeching on the pavement).

Mortgage rates have doubled since the beginning of the year, and yet rents are still rising 9% a year. (As recent as May, rents rose +18% year on year!)

While visually, it does look like rents are falling, but that was from an outlier peak of 18% in May….my personal view is anything that has growth in this world is POSITIVE!

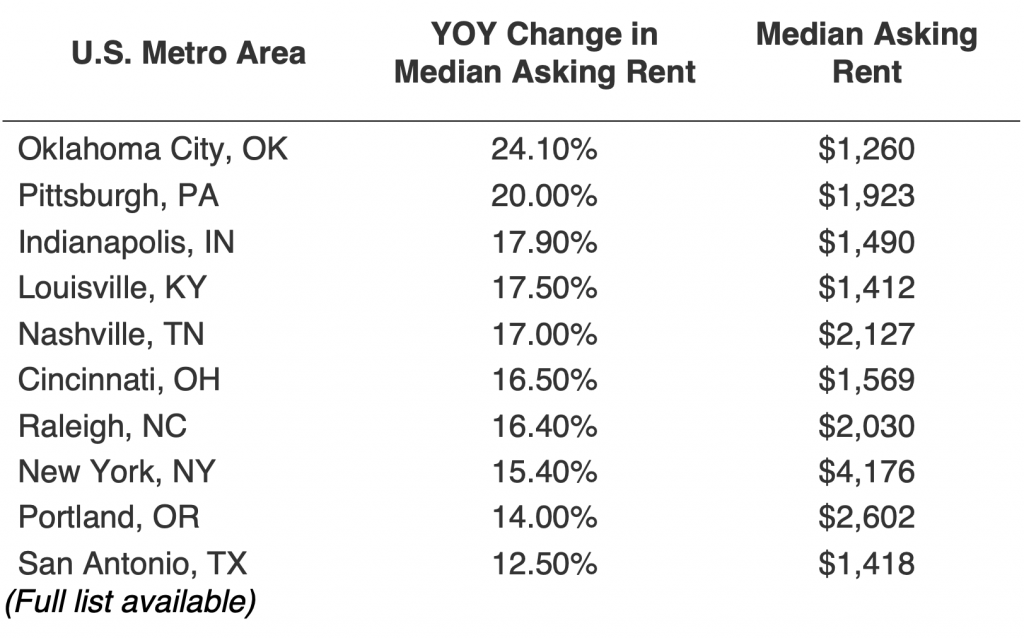

In some cities like Oklahoma City and Pittsburgh, rents rose by more than 20% year-on-year (not a typo). More below.

THE PROBLEM – HOUSING SHORTAGE

A housing shortage is not something you can really see. We hear it on the news or read it in the papers, and we think…how can that possibly be an issue.

Can't homebuilders just build more homes?

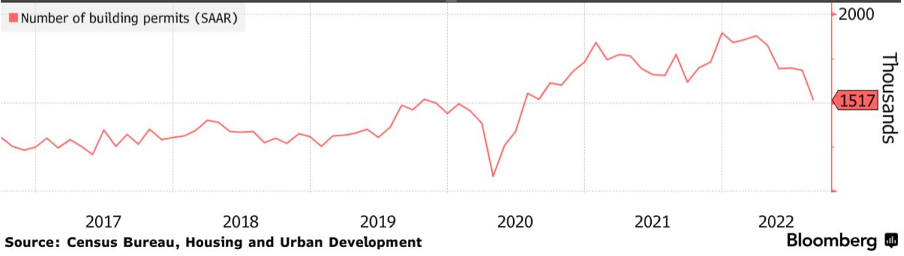

The NABM/Wells Fargo Housing Market Index dropped three points to 46 in September, the lowest reading since May 2014!

Meanwhile, "Application to Build" declined to 1.52M units, the lowest since 2020.

Number of Building Permits (SAAR)

One could also conclude with higher borrowing costs, homebuilders are discouraged from starting new projects, which is not helping the undersupply situation.

Another aspect of this is the financial incentive.

Like many other issues in the U.S. economy, there has been a focus on shareholder returns, dividends, share buybacks, etc., and hence the underinvestment in housing development since the Financial Crisis in 2008.

In fact, fewer homes were built in the U.S. in the 10 years following the 2008 financial crisis than in any decade since the 1960s! Think about that for a moment!

In the normal world, high mortgage rates tend to bring down values, and of course, there are some parts of the U.S. that are seeing a relatively faster decline in home prices, like San Francisco. I would argue that is city-specific, as the local economy hollows out and the homeless situation and cost of living is untenable for most.

Across the nation, there are indeed fewer sales and more price cuts on listed homes.

However, in this "Everything-is-weird" economy, the doubling in mortgage rates hasn't caused home prices to fall as much as you would think, all things equal.

In fact, I really don't think we are going to see any substantial collapse in home prices in the coming years because many owners bought when mortgage rates were low and can simply stay put through this phase of the economic cycle.

Also, there was less speculation, and investors put more equity in the properties during a time of tight supply. This will keep many families locked out of homeownership and forced to rent.

Here are some mind-blowing data points: Around half of all mortgages outstanding are under 4% fixed for 30 years, and about 40% of all homes are owned free and clear. Think about that for a moment!

Last month, Philly Fed President Patrick Harker discussed his recent research report with most major news outlets, "Unpacking Shelter Inflation", September 2022, that the housing shortage is a key inflation driver. Read: "…housing shortage…"

In another research report by the Fed, "Volatility in Home Sales and Prices: Supply or Demand?", Anenberg and Ringo, June 2022, write:

"We find that a 30% increase in the monthly number of homes coming onto the market would have been necessary to keep up with the pandemic-era surge in demand. Since new construction typically accounts for about 15% of supply, our estimates imply that new construction would have had to increase by roughly 300% to absorb the pandemic-era surge in demand. This is a very large, unrealistic impulse to housing supply in the short-run, suggesting that policies aimed at reducing bottlenecks to new construction would have done little to cool the housing market during Covid-19."

Read again: "…new construction would have had to increase by roughly 300% to absorb the pandemic-era surge in demand."

Here is yet another report, this time by Freddie Mac. "Housing Supply: A Growing Deficit", Kater, May 2022. I give a little more weight to Freddie Mac since they are actually buying the loans. Their thesis is that:

"As of the fourth quarter of 2020, the U.S. had a housing supply deficit of 3.8 million units. These 3.8 million units are needed not only to meet the demand from the growing number of households but also to maintain a target vacancy rate of 13%. Between 2018 and 2020, the housing stock deficit increased by approximately 52%."

Read yet again! "…U.S. housing supply deficit of 3.8 million units."

I always take stuff like this with a grain of salt because academics look at things from a 10,000 ft altitude and through the lens of an Excel spreadsheet, but the gist is that every Think Tank in the world seems to claim there is a shortage of housing supply and since they have a few more tools (and PhDs) at their disposal for this that I do, I will take their conclusions at face value.

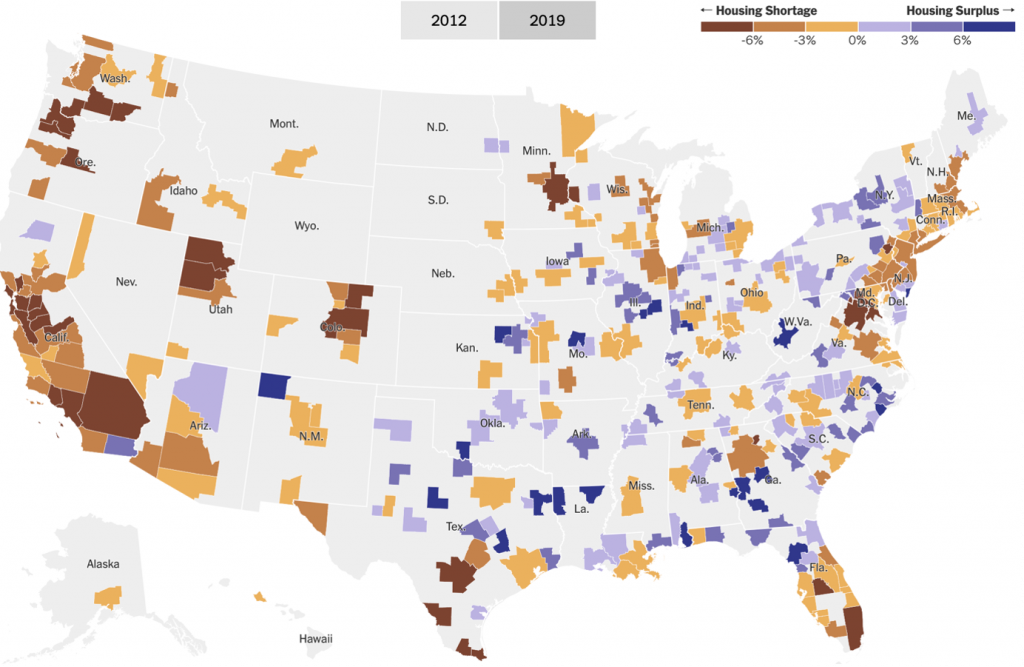

Here is a neat graphic from The New York Times, The Housing Shortage Isn't' Just a Coastal Thing Anymore" Badger and Washington, July 2022.

The Housing Shortage has Spread to More Parts of the Country.

Source: Up for Growth analysis of U.S. Census Bureau and U.S. Department of Housing and Urban Development data. Shortage percentages reflect estimated housing units needed to meet demand as a share of existing housing units. Metros with a surplus have enough housing for existing residents.

Let’s look at recent city-specific rental prices:

Top 10 HIGHEST Year-on-year Change in Median Asking Rent (%) *

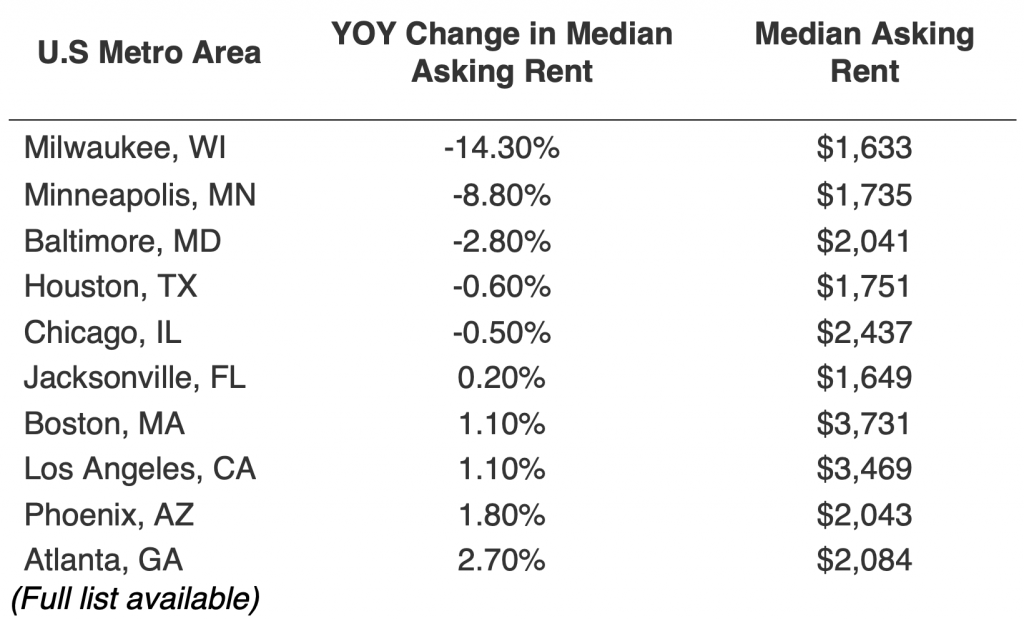

Top 10 LOWEST Year-on-year Change in Median Asking Rent (%) *

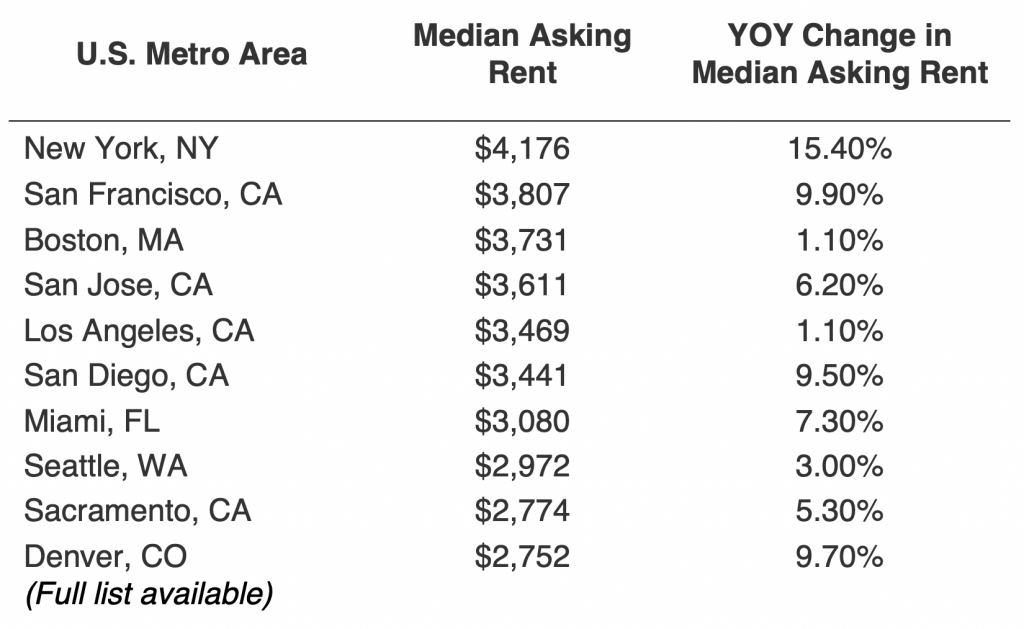

Top 10 HIGHEST Median Asking Rent *

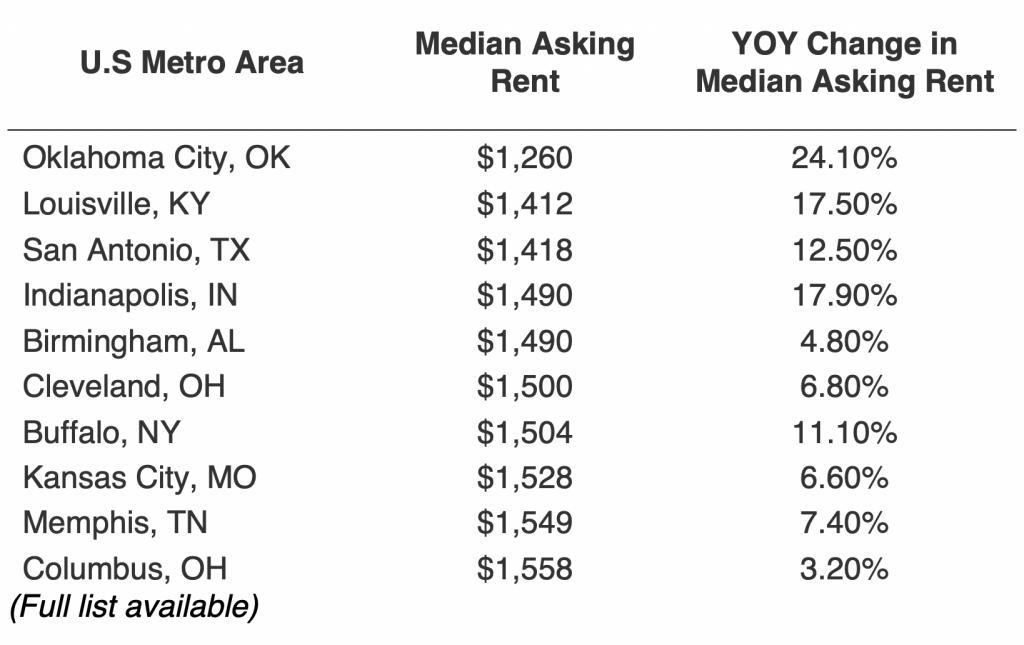

Top 10 LOWEST Median Asking Rent *

* From Redfin News: "Rental Market Tracker: Rents are Growing Half as Fast as They Were 6 Months Ago," by Lily Katz, October 13, 2022 Methodology - Redfin analyzed rent prices from Rent.com across the 50 largest U.S. metro areas. This analysis uses data from more than 20,000 apartment buildings across the country.It is important to note that the prices in this report reflect the current costs of new leases during each time period. In other words, the amount shown as the median rent is not the median of what all renters are paying but the median cost of apartments that were available for new renters during the report month. Currently, Redfin's data from Rent.com includes only median rent at the metro level. Future reports will compare median rent prices at a more granular geographic level.

DEMAND IS DIFFERENT NOW

Single-person households accounted for 80% of the new household units that have formed since 2020. Think your one-man Crypto trader or Tik Tok marketer. Meanwhile, the number of Gen Z adults living alone almost doubled from January 2020 to early 2022 (sounds like a lot of COVID breakups), likely using the stimulus income to get started. The point here is that the way labour formation is defined now makes this current real estate cycle and how it interacts with the overall economy very different from past cycles.

Another quirk of the world we live in is Video Conferencing. While we can imagine a world where we go back 5 days a week but in reality, my view is that how we work has changed forever and there are clear benefits for being able to Zoom. What this has done is artificially increased the living space needed (globally). That is to say, adding a corner or a room just for Zoom calls etc, driving up demand for overall living space.

SUMMARY

In summary, the makeup of the labour market, as well as the supply demand imbalances in real estate, are very supportive of higher rental prices and rental yields over the long term.

As a non-resident buyer of U.S. real estate hoping to earn income, this is the perfect storm and has only happened BECAUSE rates are rising.

We may see rates come down in the future where borrowers can easily refinance into a lower rate, but what if prices do not come down or there is a sudden price surge next year? These are all crystal ball-type guesses but what I want to leave with you in this report is that the lack of supply is a major long-term driver of higher rental yields, which is positive for any U.S. real estate investor.

U.S. real estate is considered a safe haven for many – low entry price point, no stamp duties, ease of gentrification, available tax deductions, USD income, ease of travel, quality of schooling, and the list goes on.

If you have any questions about this report or about anything U.S. real estate or mortgage related, please feel free to reach out to me directly at: +65 9773 0273 or email me at donald@gmg.asia.

The worsening energy crisis in Europe has taken the front page of most media channels this week as the Nord Stream 2 pipeline, a 1,200 km natural gas pipeline from Russia to Germany, remains close, which is driving the Euro to a 20-year low vs. USD. The BBC reports that the annual energy bill for a typical UK household is £1,971. From 1 October, however, that's due to rise 80% - to £3,549!!! Can you imagine paying USD4,000 a month for electricity?! The new incoming PM, Ms. Truss, will certainly be making this a top priority. We really hope for a mild winter in Europe for everyone's interest.

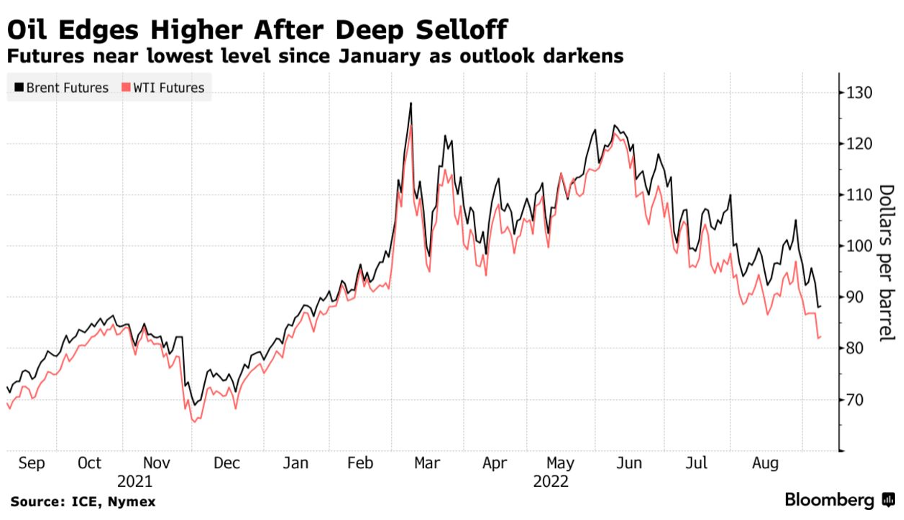

Meanwhile, the Yen is now close to a mind-boggling ¥145 vs. USD, a 24-year low! Oil at $82 is a very critical level and, technically speaking, could break lower, which could give some breathing room to the economy. Seeing Oil go from $120 a barrel in May 2022 to $85 now shows how volatile the world is and also how quickly demand can fall for the most popular commodities.

In the US, Nonfarm payrolls were +315,000 in August (seasonally slow) vs. +526,000 in September, slightly lower than expected but a big month-on-month decline. Meanwhile, unemployment is at +3.7%, slightly higher than expected. The tight labour market while companies are announcing hiring freezes is peculiar. Could this be a recession where employment is less affected? ISM Manufacturing for August was 52.8, unchanged from July – not the decline I was hoping for to give us a little breathing room.

* Reference only. These rates are Conforming rates, not applicable to Foreign Nationals.

Ex-ante

I'm really keeping an eye on oil prices…I have a sinking feeling that Oil is such a consensus overweight for most hedge funds (and institutions) that technical breakthrough support (say $80) will see a further decline in oil prices which is good news for everyone! European energy prices are now generally 15-20% of GDP, and someone has to pay for it – the public or private sector. If the public pays for it, it will have to run a fiscal deficit of 15-20% of GDP, so more debt on top of the already growing debt problem. The private sector gets tricky, especially for countries that have piled on loads of debt in a short period of time. One country that sticks out is Sweden, with over 150% of private debt to GDP. Nationally, Sweden's debt service ratio is 27% (highest on record). It appears Sweden, France, and South Korea are the most interest-rate sensitive countries, relatively speaking, according to BIS data. Watch this space. The negative soundbites on the European banking sector are going to get louder and more frequent.

Buy now! Why now?

We are in a perverse cycle where rising rates are actually squeezing up rental yields. The marginal buyer cannot afford to own given rate rises, and the Millennials also cannot afford and must rent – AND, to add to that, there is a 3.8M housing shortage according to the Fed. If you read last week's "Ex-post, Ex-ante," places like New York are seeing double-digit percentage increases in rents, BUT 39% of residents are looking to move given the high cost of living. It won't be long where we are in a world where rates are 7-8%, BUT rental yields could be 15-20% (some parts of Texas can net you low teens yield already).

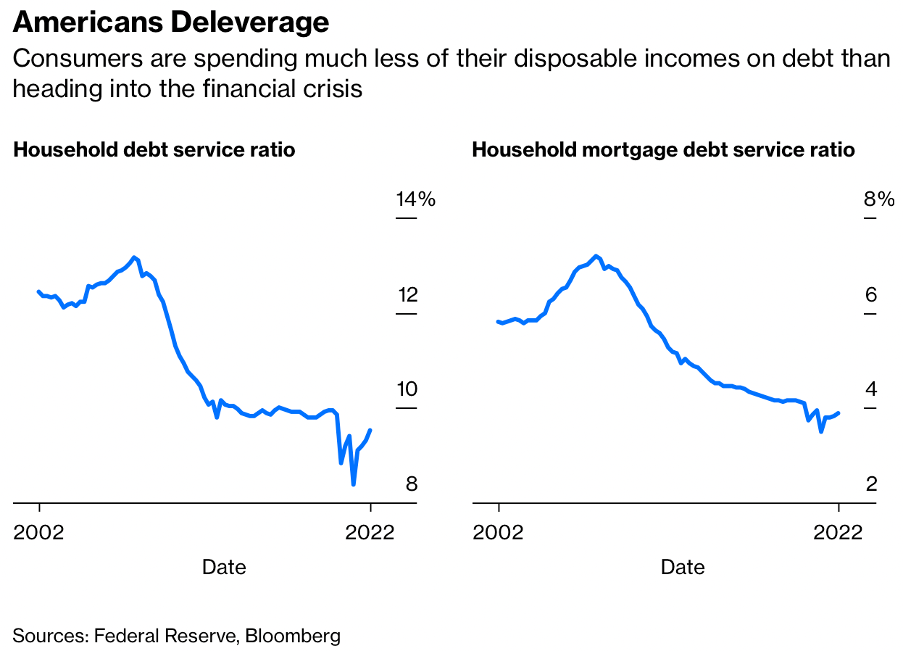

Look at this chart below from a Bloomberg article (7 September) US household debt service ratio has fallen from around 13% at the time of the last housing crisis to 10% now, according to the Fed. The amount households are spending to service their mortgage debt has been cut almost in half, from 7.18% in 2007 to a recent 3.89%!

LOANS OF THE WEEK!

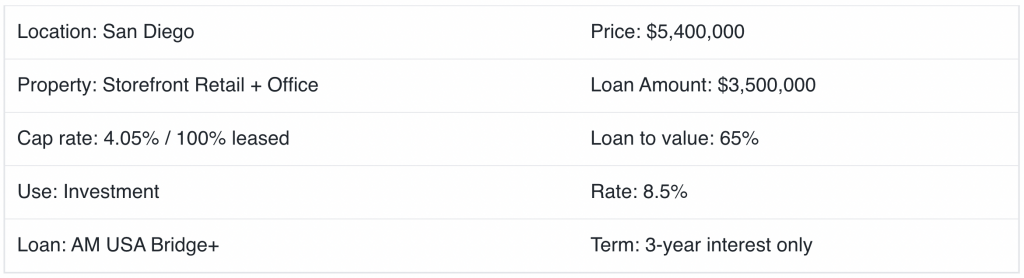

1. Indonesia family uses bridge loan to purchase $5.4M Retail/Office to maximize cash flow

- Client was offered a bank loan at 5.75% but given that it is cash-flow based he would not be able to cover the 1.25x cash flow coverage typically required and would be able to get around 40% LTV. Our knowledge was valuable. We knew that California is a tough market as it is with very low CAP rates but the added increase in interest rates is making it even harder to achieve higher loan amounts.

- Our solution: Use a bridge loan with higher leverage, interest-only payment to get into the property. Then position the tenants for renewal of their lease agreements and refinance when rates come back, allowing for more leverage to be supported by the cash flow. Good news is the client is using this strategy to purchase more yielding assets in the US. Loan managed by our Head of Sales, nick.worthing@americamortgages.com

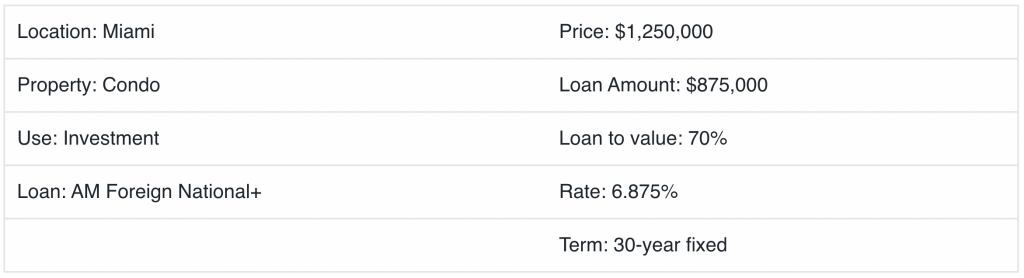

2. Canada tech entrepreneur buys $1.25M condo in Miami

- Client wanted to start building rental portfolio in the US to earn income and to begin developing a credit footprint for future family and business opportunities. Given the nature of his business, he was not able to find bank financing in Canada and we were able to find a mortgage which used his Canada credit and income to qualify. Funded in 43 days with the help of our Canada-based loan officer, kristen.young@americamortgages.com

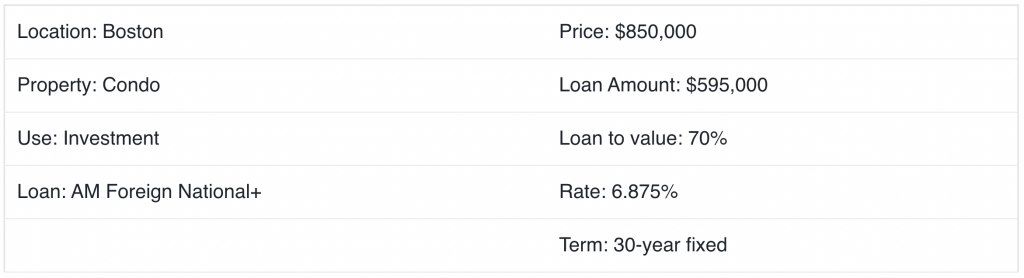

3. UK family buys $850K Boston condo in son’s name to develop credit

- Client bought condo in son’s name to rent out while his son attends boarding school on the East Coast. The intention is for him to stay in the condo upon graduation from university in 4-5 years or continue to rent out to bolster his income while starting out on his career, meanwhile developing US credit for himself. Our UK-based loan officer provided a hassle-free experience throughout their mortgage journey, diana.gomez-mcgurk@americamortgages.com

Schedule a call with us at hello@gmg.asia to find out more!

Biden cancels $10,000 in student debt – timing before the mid-term elections are interesting, but no one can deny that it is a big problem that is stifling growth in many ways. The main event was Federal Reserve chairman Powell’s speech at Jackson Hole, which was a reminder that inflation is being treated more seriously than we are expecting. Risk assets have been correcting ever since – yet bonds haven’t moved with the same intent indicating smart money had priced in the Fed’s response. While 10Y treasuries do not dictate mortgage rates, they 2 are correlated, and we expect some upward pressure on rates.

Ex-ante

Over the next week, we will be paying attention to the Case-Schiller index as a gauge of year-on-year home prices, and the big one is August ISM manufacturing index, which consensus has at 51.8 (under 50 is a contraction). If this is lower than consensus, it may portend to be something more recessionary. As we highlighted in last week’s “Ex-ante, Ex-post,” there is historically a big contraction in manufacturing output when rates rise to a certain extent.

US HOME PRICES

We reiterate the underlying fundamentals of housing are very supportive, with an abundant amount of equity and well-known shortage.

In an article written by the Fed, on 7 May 2021, “Housing Supply: A Growing Deficit”, they claim in 2018, the housing shortage was 2.5 million units, and now, more recently, in 2020, the US has a housing shortage of 3.8 million units.

That is to say, 3.8 million units are needed to not only meet the demand from the growing number of households but also to maintain a target vacancy rate of 13%. Between 2018 and 2020, the housing stock deficit increased by approximately 52%.

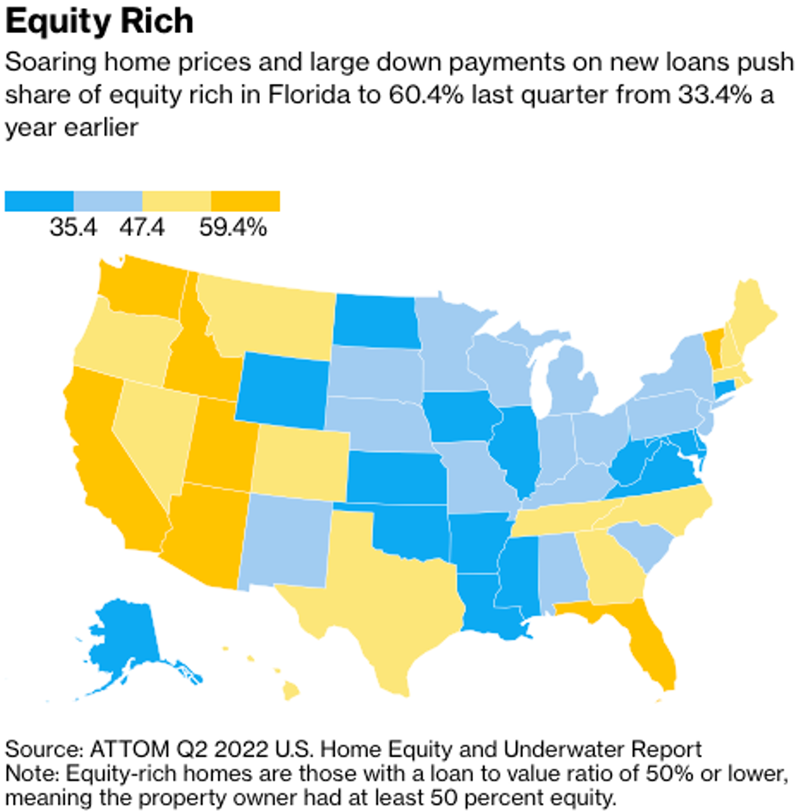

Elsewhere, In Bloomberg’s article published, 5 August 2022, “Almost Half of Mortgaged Homes in US Now Considered Equity-Rich .”This would be the 9th straight quarterly rise, according to the article, fuelled by strong house valuations during the pandemic area. The article definition of Equity-Rich as owners having over 50% in home equity. Some of the highest equity-rich states are Florida, California, Washington, Utah, Idaho (surprising), and Vermont.

LOANS OF THE WEEK!

Singapore citizen purchases new development in Manhattan, New York

Singapore client attended a presentation by an international realtor on a New York condo launch. America Mortgages was attending the event and helped the client discuss the financing options available.

Philippines businessman purchases home in Florida

Referred by his local private bank, the client wanted to own a retirement home for the future (he’s only 58) but liked how rental rates have been rising in the area and also wanted more USD income.

Swedish National purchases home in Texas

Swedish client saw our ad on LinkedIn and reached out to discuss the financing options for a Texas property. He was surprised at how easy it was to qualify and close for direct US lending option.

Interested in releasing equity or to find out more? We have a 97% approval rate for both U.S. Citizens & Foreign Nationals. Schedule a call with us at hello@gmg.asia today!

In that report, we looked at the top 50 Public, and Private high schools, average ACT/SAT scores, Median Household Income, Average Home Prices, and Rental Yield.

We argued that when looking at where to make your US property investment, the quality of education in the nearby city/area is a factor in the decision since there is always a notion of "can I live there one day" and "maybe my children can go to school there". Popular cities in the US will undoubtedly have good schools in the city or in the vicinity.

"Popularity as a living destination" in turn drives demand, home value appreciation, and strong growth in rental income.

This week we focus on Demographics.

An under-appreciated factor in determining where to own is what city has the most culturally similar population. It's much easier when you have neighbors that speak your language and share similar cultures and values.

We will answer these questions (and much more)!

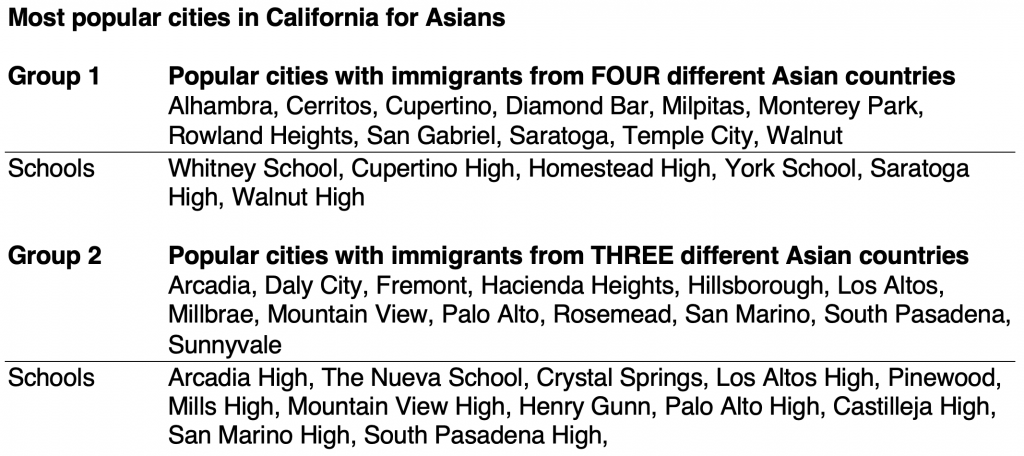

Which high schools in California has the highest Asian population?

Which cities have the most Korean-born residents?

Which cities have the highest total Asian population and the respective top schools?

Does the highest Asian population determine how home prices will behave?

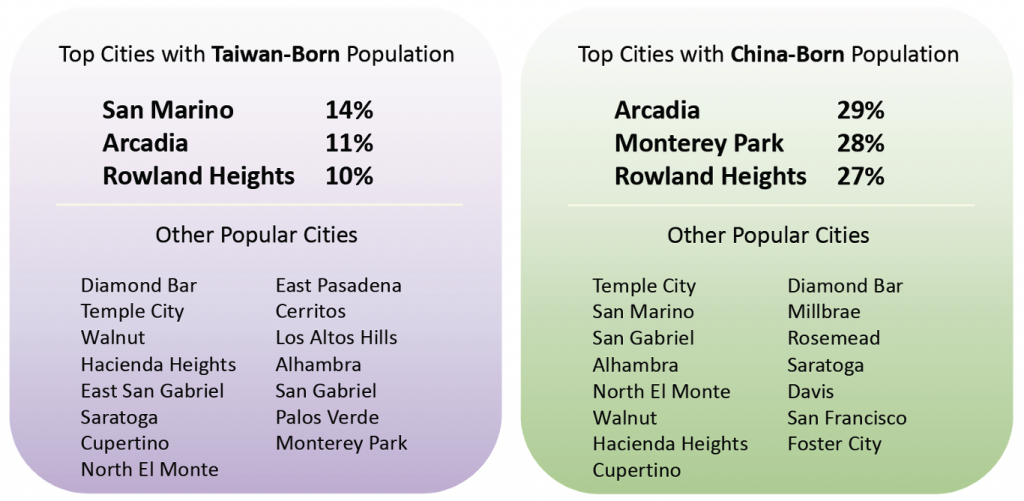

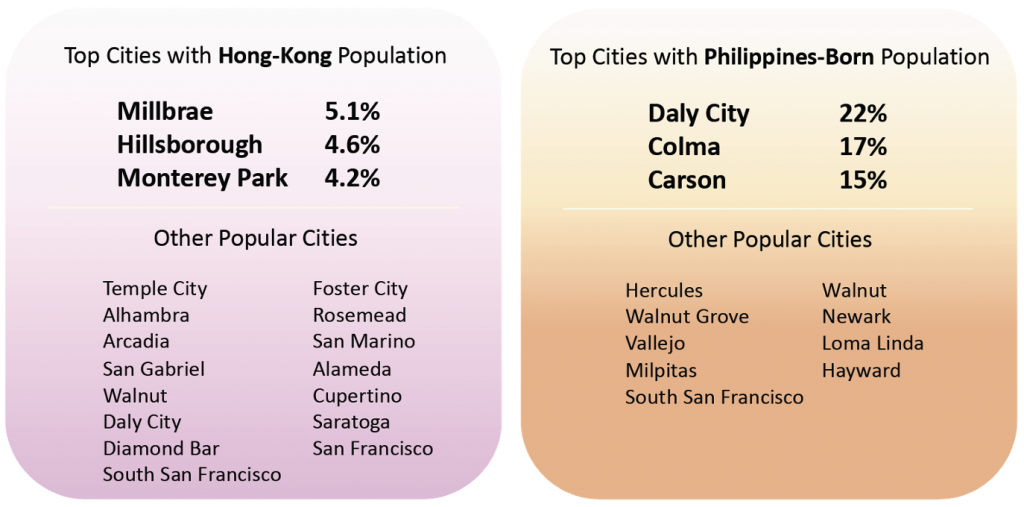

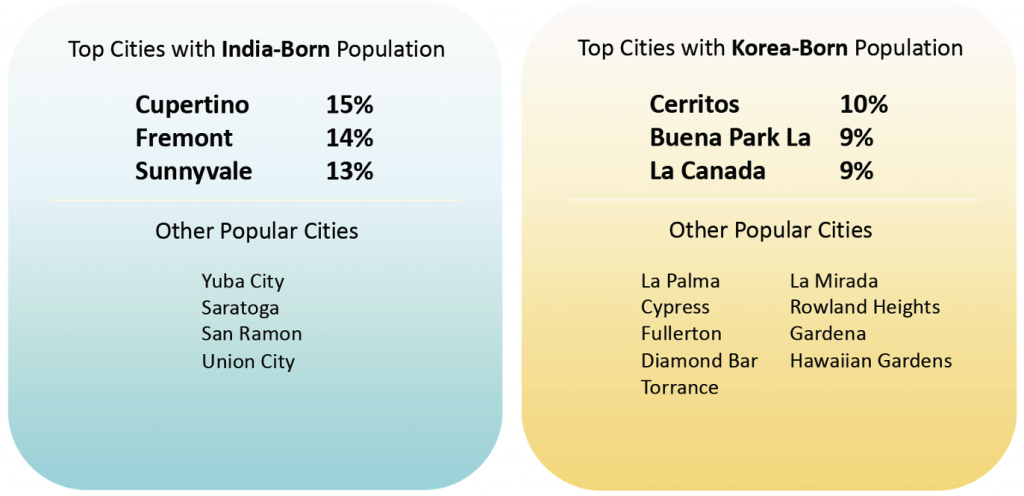

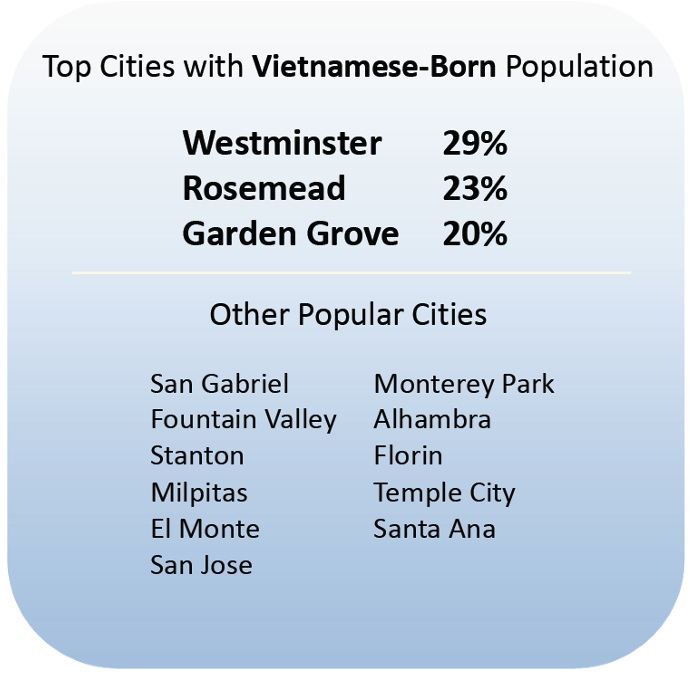

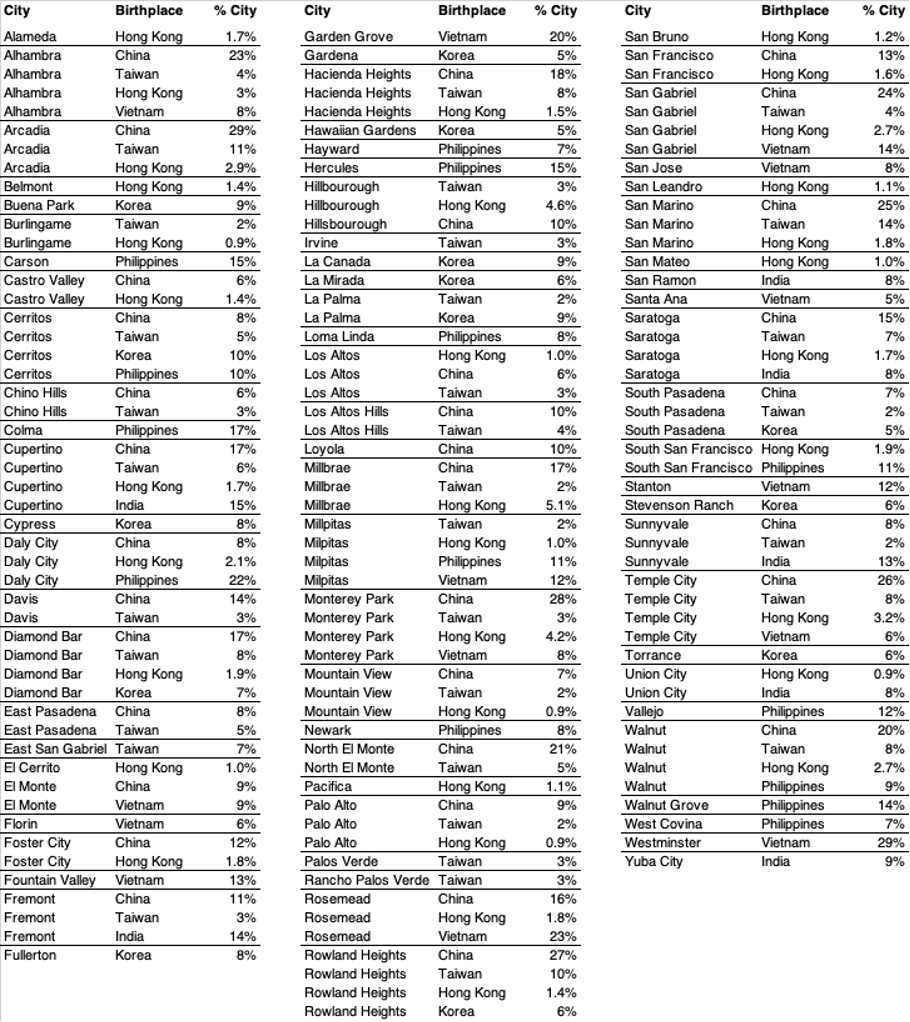

Which California cities have the highest: Hong Kong, China, Taiwan, India, South Korea, and Philippines-BORN residents?

Demographics matter!

In this study, we solely focus on the Asian population in schools. Asians have been the biggest group of immigrants over the last 60++ years, spurred mainly by the Immigration Act of 1965 but also the Taiwan Relations Act of 1979, the Luce-Celler Act of 1946 as well other obvious political issues of the time.

In addition to the above reasons, many immigrants just wanted a better life for their families, they studied hard, and slowly communities grew around the top education destinations.

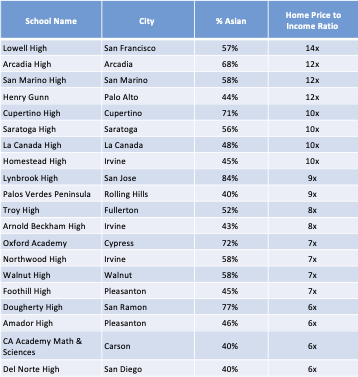

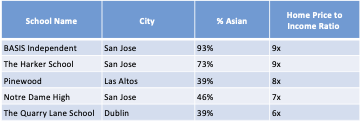

Here is the Asian population (>40%) for the top 50 Public and Private Schools in California.

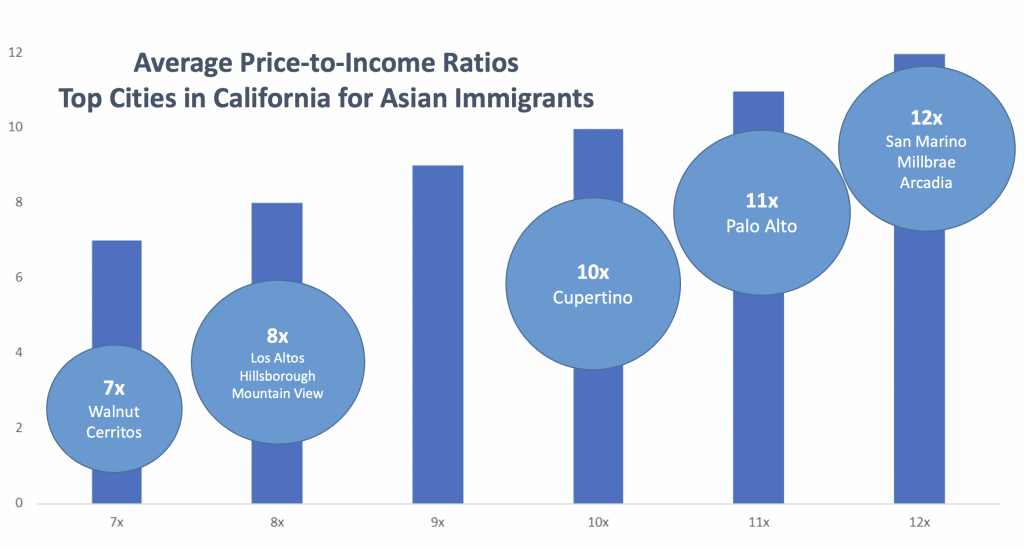

You can also see that these cities have the highest Home Price to Median Income ratios, highlighting the center of attraction for Asians moving to the US.

Note a common rule for affordability is for a home price to be UNDER 3x your income!

Public High Schools

Private High Schools

Takeaway - You can see cities where the top schools are located have very high Home Price to Income Ratios which highlights the property value growth driven by families moving to these cities, in particular Asians.

The next study is very interesting!

Our team looks at which California cities have the highest overseas-born residents, specifically from: China, Hong Kong, Taiwan, South Korea, Philippines, Vietnam, and India.

You guessed it, many are in the cities where the top schools are

We only used cities with over 20,000 population.

*Refer to full chart below

Here is same chart in Alphabetical Order

Illustrating popular cities ranked by multiple demographics

As you may observe in this report, the cities with the highest Asian immigrant population tend to be where the most demand is, especially when compared to household income, and it's no surprise it's also where the top high schools are.

That is to say, the schools and cities mentioned in last week's report on Education being the main driver of price appreciation and rents are very similar to the cities mentioned in this report.

While this study is not meant to be a rigorous analysis by any means, it is close to my heart since I moved from Singapore to San Francisco when I was 16. My parents had the same thought process…strong Hong Kong population and good schools. I ended up finishing high school in San Francisco and attended UCLA.

Stay tuned for the final part of our Buyer's Guide to California, where we take a quick look at the general carrying costs for a rental property, including taxes, deductions and other administrative costs.

Finally, we will be hosting a webinar with our California Partner for a real "on-the-ground" discussion along with a panel of real estate experts for the Bay Area, Palo Alto, Los Angeles, and Orange County. We are still finalising the exact details, but this will be in September.

Have a good weekend! If you want a copy of the spreadsheet with the data from our research, please contact us. We are happy to share our findings.

Welcome to our newly revamped weekly product, where we do a quick summary of salient news over the past week and what to expect the following week and beyond. It took a while to think of a catchy name for our weekly and we hope you like it. We also plan to include our house view of the major macro events and, of course, how it all relates to the global real estate markets, in particular the US.

Contents:

Ex-post; Ex-ante

Will rates decline? Yes, starting in March!

Why US home prices will not collapse

Buyer’s Guide to California

Loans of the week!

Ex-post

Last week saw major headlines with UK printing a 10% inflation number and Europe continuing to see hefty price increases in energy costs, with Germany at €700 ($696) a megawatt-hour, up from under €50 in January.

In the US, mortgage applications dipped slightly for the week ending August 12, 2022, down 2.3% week on week. Things are generally slower in all areas of the economy in August, and this is no different.

30-year fixed rate 5.45% mortgages are down 50 bps from June 2020 highs of 5.98%

* This reference rate is for conforming Fannie Mae loans, not applicable for overseas borrowers.

Ex-ante

This week, all eyes will be on Jackson Hole, where Fed chair Jerome Powell will speak on the economic outlook at 10 am Washington time. We cannot see Powell becoming incrementally dovish at this stage, while there could be an outside chance of being less hawkish. As a firm, our house view is that given the fact that the “reputation and credibility as an institution” is under pressure, the Fed will risk over-tightening in this economic cycle – right or wrong. To us, tightening into a recession is extremely heavy-handed, but Powell certainly does not want to be remembered as Arthur Burns 2.0.

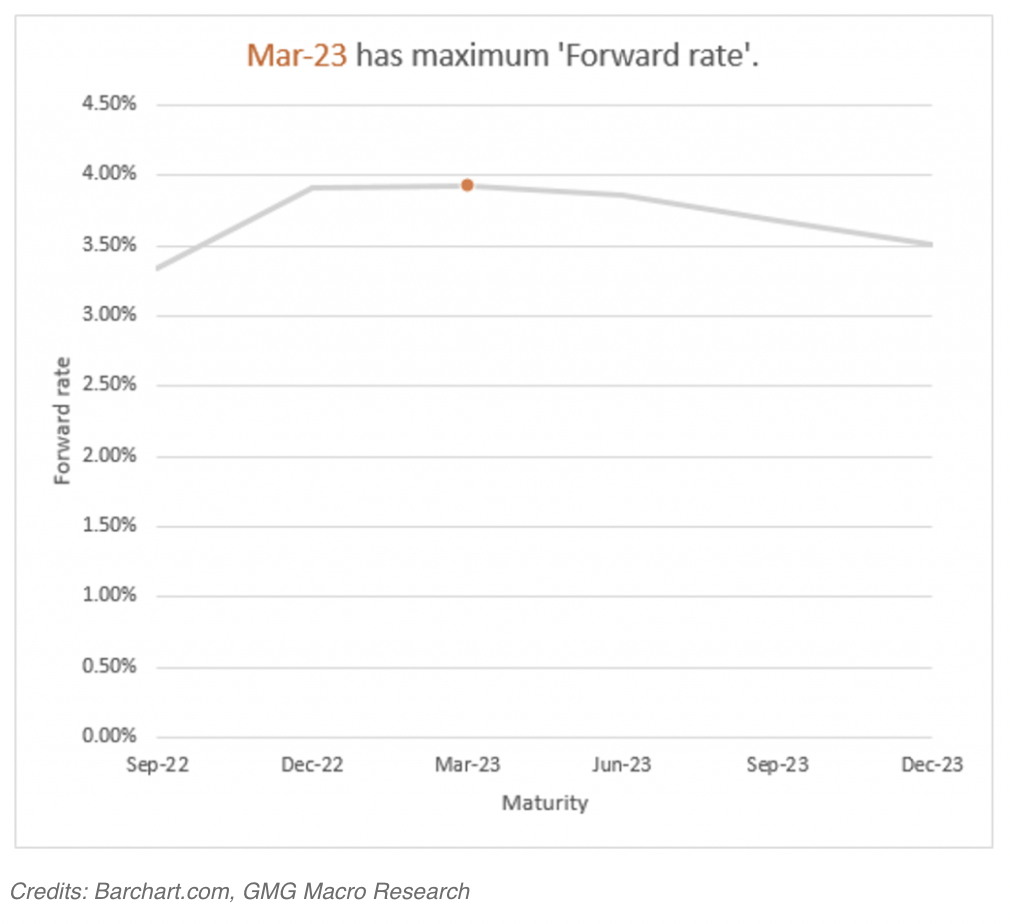

The Trillion-dollar question is IF rates will be cut, and if so, how much?

If you look at the Eurodollar implied futures curve, you will see that the market is expecting rates to peak in March 2023 at 3.93% and then start to decline to 3.51% by December 2023, and drop to 3.03% a year later. That is to say; the market is expecting 90 bps of decline in Fed Funds by December 2024! The charts also imply that rates are expected to stay under 3% thereafter.

3-month Eurodollar Futures Yield Curve

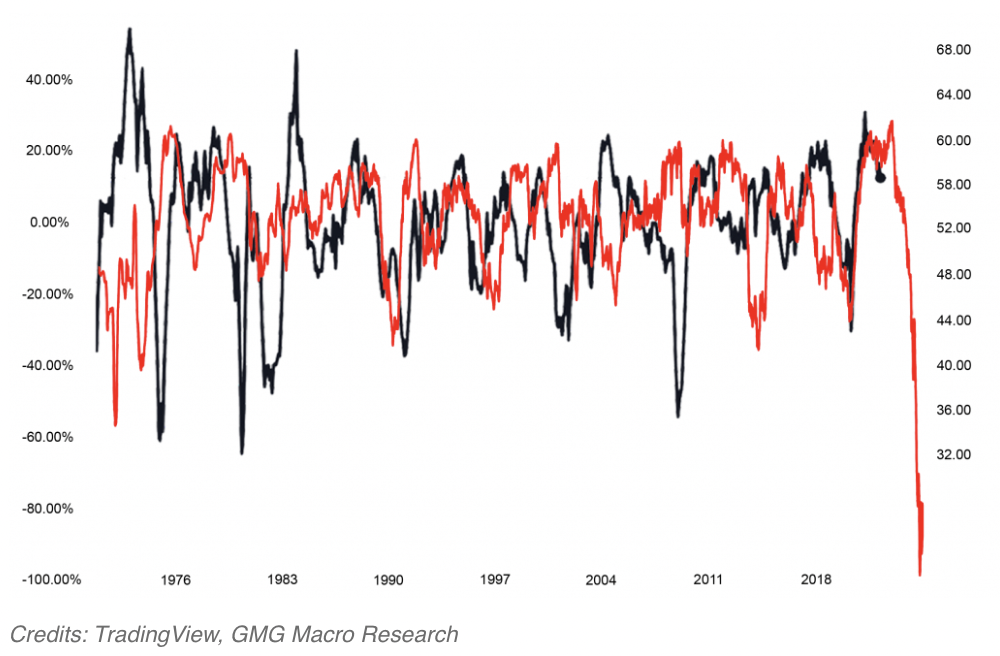

ISM Manufacturing Index - US 30-Year Mortgage, YoY%, 18-Month Lead Inverse"

One area of potential concern is US industrial production, which is at risk of significant contraction (below 50 on ISM Manufacturing Index is a contraction). If so, this could trigger deeper recession concerns. The next the Institute of Supply Management (ISM) report will be out September 1st.

If you look at this chart, it appears that the ISM Manufacturing Index (black line) lags the inverse of the US average 30-year mortgage rates (red line) by about 18 months. If the US manufacturing economy pans out in this manner, the Fed may be forced to make deeper cuts and we could see a bigger decline in rates than the market is pricing in, giving another opportunity for US home buyers who are waiting for lower rates!

Home Prices

There is no impending collapse. We see strength in housing prices.

As we read in the media that home prices are softening, housing starts declining, home prices are falling, and it paints a doom and gloom picture, but we cannot see a collapse in housing prices and a repeat of 2008.

Did you know that 40% of all homes in the US are held free and clear without a mortgage?

The average outstanding mortgage is 33% of home values. There is simply too much equity in the market for a collapse. Since 2008 underwriting standards have been significantly more stringent with more regulatory oversight. More importantly, most of the outstanding mortgages were printed when rates were below 4%!

Sure, in some cities, there will be softening as residents gentrify out to lower cost of living areas. It’s no surprise that San Francisco, Los Angeles, and New York City are at the tops of those cities where there are significant outflows of residents.

According to a Redfin article on July 18, 2022, here are the:

Top outflow cities in 2Q2022:

Top inflow cities in 2Q2022:

Buyer’s Guide to California

Over the past 2 weeks, we have published a Deep Dive into what drives overseas buyers to California. In Part 1 – Education.We look at the top 50 public and private high schools in the state, average SAT/ACT scores, Median Income and Average Home prices and conclude the cities with the top schools tend to have the strongest property price appreciation and rental reversions.

In last week’s Part 2 – Demographics.We look at the Asian population in each of these schools and conclude the schools with the highest Asian population is another driver of home prices where the top schools are located.

This week, in Part 3 – Taxes and Benefits. We will conclude the report with a tax guide for overseas investors, how rental income is taxed and various deductions that are allowed.

Finally, to wrap-up our Buyer’s Guide to California, we will be hosting a webinar with Susan Kim, our Private Client US Concierge Partner and top real estate experts in San Francisco, Palo Alto, Los Angeles, and Orange County to give you an on-the-ground discussion on the respective cities, where the value is now and in the future. Stay tuned!

Loans of the week!

1. Switzerland Family Office purchases luxury condo in New York

Client wanted options outside of their private bank which did not require pledging assets.

Type: Luxury Condo

Price: $20M

Loan Amount: $11M (55% LTV)

Use: Second home

Loan type: America Mortgage HNW+

Qualification: Using borrower’s liquid investment portfolio as a reference without encumbrances. (Example Fidelity account)

Term: 5-year fixed / 30-year amortized

Interest-only: Fixed for 5 years

Rate: 7.875%

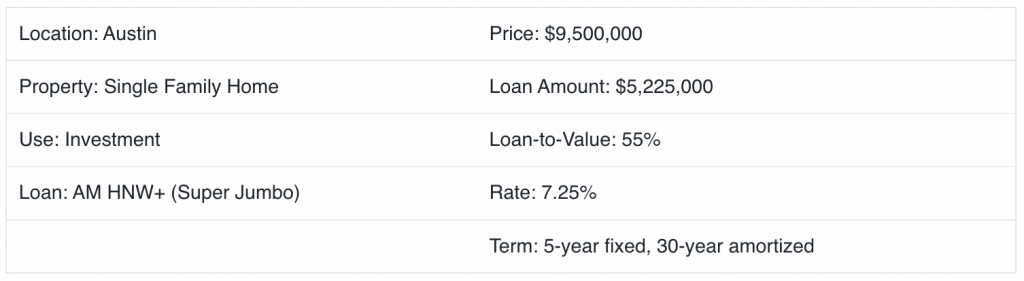

2. UK technology entrepreneur purchases home in Atherton (near Palo Alto)

UK-national client attended Stanford and plans to move their children there in 3 years to attend high school. His goal was to rent out the home to tech executives or AirBNB in the interim.

Type: Single-family home

Price: $10.9M

Loan Amount: $6M (55% LTV)

Use: Investment

Loan type: America Mortgage HNW+

Qualification: Using borrower’s liquid investment portfolio as a reference without encumbrances. (Example Fidelity account)

Term: 5-year fixed / 30-year amortized

Interest-only: Fixed for 5 years

Rate: 7.25%

3. Singaporean family purchases home in San Antonio for rental income

Father attended the University of Texas and, after reading our Deep Dive report, decided to own a home where he could take advantage of the strong USD and rental income currently in San Antonio and potentially will move there for retirement.

Type: Single-family home

Price: $350,000

Loan Amount: $245,000 (70% LTV)

Use: Investment

Loan type: America Mortgage Foreign National+

Qualification: Based on overseas income and credit

Term: 30-year fixed

Rate: 6.875%

Thank you and feel free to contact us if you have any questions.

We are super excited to kick off our "Buyer's Guide to U.S. Real Estate" series, where we go in-depth into the main U.S. states for property investment purchases, starting with California!

We also have a surprise guest at the end of the month (see bottom of article)!

What's not to love about the Bohemian vibes of San Francisco, the technology center-of-the-universe in Palo Alto, wineries in Napa, food in Yountville, golf in Steinbeck country, the quaint and exclusive Montecito, and year around perfect weather in San Diego.

And finally, Los Angeles – Beverly Hills, Hollywood, Venice Beach, Santa Monica, Bel Air, Pasadena, Orange County – it's almost endless.

It's no surprise that California is a favourite investment destination for our clients, both Overseas Expats and Foreign Nationals, primarily from: the U.K., Canada, Australia, Mexico, China, Hong Kong, Singapore, Philippines, Indonesia, Australia, France, UAE, Germany to name a few.

Want Home Value Appreciation and Rental Income Growth?

Education is key!

Job market growth is certainly a key driver for price appreciation and is normally driven by the new business formation in the area, but popularity as a living destination is driven by things like safety, cost of living, ease of transportation and quality of education, especially for families with young children.

"Popularity as a living destination" in turn drives demand, home value appreciation, and strong growth in rental income.

Why is Education important?

In this week's report, we will take a deep dive into Education – an important (if not the most important) factor for overseas property investors in determining where your next home purchase will be in the U.S.

With Foreign National buyers, in particular, the objective of owning real estate to earn income almost always comes down to "could I live there one day"?

In Asia, where owning property is ingrained in their culture, it's common to purchase an investment property "in anticipation" of sending their child to college. They could even live there during or after they graduate, and the price appreciation could even pay for college if they sell the property. Or, if the child decides to get a job in the U.S., they can stay in the apartment as a post-graduation gift to build up their credit or even rent it out to earn income.

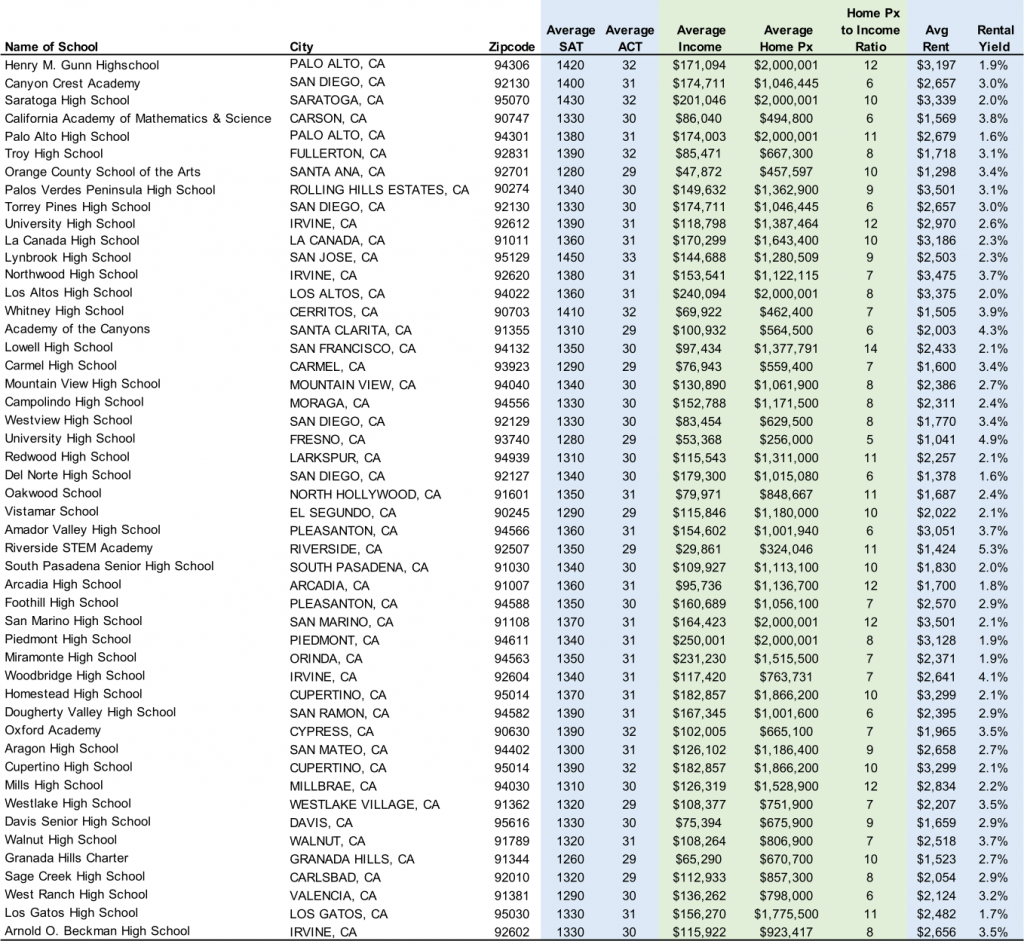

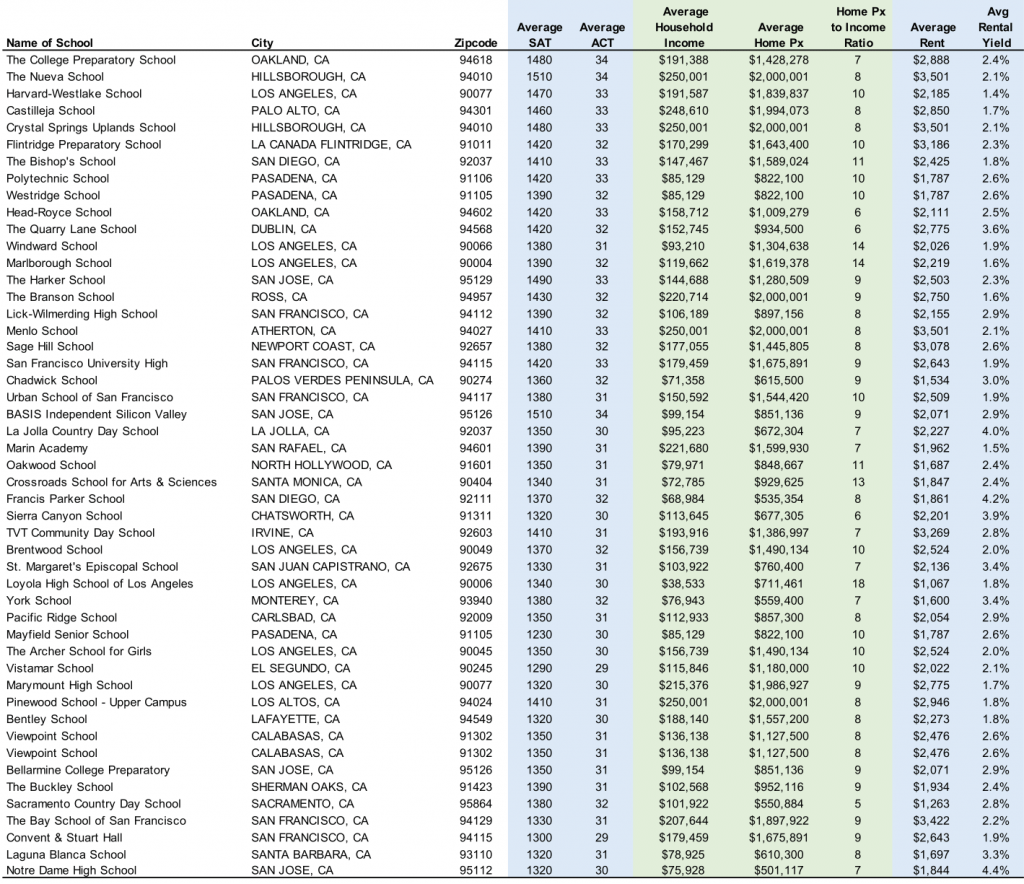

Which are the top high schools in California?

We look at the top 50 high schools in California, both public and private, ranked by average SAT and ACT scores. As you can see, the SAT scores will range from 1300-1500. To get into a top 25 U.S. university, the SAT scores should be at least 1400 as a reference, so these schools are all great.

Why high schools?

Many new immigrants or returning expats will choose to live in areas where there are good schools and a higher population of similar background families (the latter we will investigate next week). High schools are a very important decision since it will determine their experience during these formative years between 14-18 years old but also potential college choices.

"Popularity as a living destination" drives demand, home value appreciation, and strong growth in rental income.

Schools with the highest SAT/ACT scores

- Public: Lynbrook High School, San Jose

- Avg SAT 1450 / ACT 33

- Private: The Nueva School in Hillsborough & Basis Independent in San Jose

- Avg SAT 1510 / ACT 34 for both

Household Income, Home Prices, and Rental Yield

We also look at the Median Household Income, Average Home Prices, and Rental yield in each city. When moving to a new city, aside from the quality of education, most will look at how expensive it will be to live there, own a home, and potential rental income potential.

It's probably no surprise cities like Palo Alto, San Diego, San Jose, Los Angeles, and others will have higher home prices, but we also look at a rough gauge of affordability which is a "Home Price to Income Ratio," which tends to be where most immigrant buyers choose as their base.

Cities with the highest Median Income

- $250,000+ per annum income

- Cities: Piedmont, Hillsborough, Los Altos

- Neighbouring schools: Piedmont High School, Los Altos High

Cities with the highest Home Prices

- $2,000,000+ home price

- Cities: Piedmont, Palo Alto, Hillsborough, Ross, Atherton, Los Alto, Saratoga, San Marino

- Neighbouring schools: Piedmont High School, Los Altos High, Palo Alto High, Henry Gunn, Aragon High, Nueva School, Crystal Springs Uplands, The Branson School, Menlo High, Pinewood School, San Marino High

Highest Rental Yield

>5% gross yield: Riverside >4% gross yield: Lo Jolla, San Diego, San Jose, Fresno, Irvine, San Clarita

- Neighbouring schools: Riverside STEM Academy, Canyon Crest Academy, Torrey Pines High, Westview High, Del Norte High, The Bishops School, La Jolla Country Day School, Francis Parker School, The Harder School, Basis Independent, Bellamine College Prep, Notre Dame High, University High Fresno, University High Irvine, Woodbridge High, Arnold Beckham High, TVT Community Day School, Academy of the Canyons

America Mortgage Concierge Program

We launched this free service last month to connect potential home buyers with our approved panel of realtors in each major U.S. city, which only focuses on overseas buyers. If you would like to learn more, please contact james.morales@americamortgages.com.

Our surprise guests!

At the end of August, we will be hosting a webinar with our California partner, who will present a "Guide to California Real Estate" along with a panel of the top realtors in Los Angeles, Orange County, and Bay Area to give you a real "on the ground"feel for all the points we discussed above and more.

Stay tuned…this is going to be amazing!

Sources: Niche, City-Data, US News, OECD data, US Census Bureau and respective school websites

Globally, but especially in the main overseas investor markets like the US, UK, Canada, and Australia, the housing market has seen intense competition, massive price surges, and dwindling inventory since 2020 - but if you're a real estate investor, all of that may be about to change, and for the better.

Using the US as a reference, mortgage rates are rising. In mid-June of 2022, the 30-year fixed-rate mortgage averaged 5.81%. That may seem high; however, rates now are where they were right after the financial crisis of 2008 when many people were actively trying to obtain a mortgage.

What makes this type of market great for real estate investors?

These higher rates make it more difficult for would-be home buyers to afford new homes. It's not that people are trying to buy extravagant houses, but that a modest home with an increase of $50 a month in mortgage payments could be the difference between buying or renting.

These higher costs are putting pressure on the housing market. It has already led to a decrease in mortgage applications to purchase and refinance for owner-occupied property, but an increase in investor mortgage applications getting in on high rental prices, demand, and lack of available rentals.

What once was a seller's market is shifting slightly, causing properties to stay on the market longer. This has resulted in liquidity issues for investors looking to sell their properties quickly to buy additional properties.

Luckily, there is a relatively simple and easy financing solution - GMG bridge loans.

What is a Bridging Loan?

Investors use real estate bridge loans as a short-term financing tool to bridge gaps in financing. For example, an investor might take out a bridge loan against a property they are selling in order to purchase or act on another investment property immediately.

In this case, the homeowner may need the money before their property sells. They can now use a GMG Bridge loan to extract equity today while waiting for the right price to sell.

Bridge loans can be secured quickly, often closing within a week to 10 days, and with little paperwork, because lenders are more interested in the collateral (i.e., a house) than a credit score or cash flow.

We offer Bridging Loans in: USA, UK, Canada, Australia, Singapore, Hong Kong, and Thailand.

How to use Bridging Loans to free up liquidity

Bridge loans allow investors to quickly free up liquidity using their real estate assets as collateral. This is a quick asset-backed mortgage where your financials or credit are not the primary underwriting criteria; the asset is. In order to better understand how this works, let's take a look at two examples;

1. Waiting for a property to sell at the right price:

You're selling a property but waiting for the right price. Another investment property becomes available that is too good to pass up, but you won't have the available funds until after you sell the existing property. No problem. Extract the equity from the property you're selling. Take advantage of the new investment. Wait for your property to sell and pay off the bridge. It's that easy and quick!

2. Financial strain:

Often, unpredictable circumstances can impact our financial position. The equity in your property can be the perfect way to ride out the storm without worrying if you'll qualify for a "conventional" mortgage loan. It is easy, quick, and straightforward to release up to 70% equity from your property based on the asset value alone. We can also structure these loans to where you do not have to make any monthly debt servicing for up to 12 months. This allows you to get the liquidity you need and then relax, reset and focus on your situation at hand.

When do Bridging Loans benefit investors?

As explained above, bridge loans are a great way to free up liquidity. A bridge loan may also be a good fit for you if you:

Need to free up liquidity in a fast-moving market

Can't afford to take out a mortgage on a new property without selling your other property.

Need to secure funds to acquire or renovate real estate quickly.

Already purchased a property, but you can't sell your current property quickly enough.

Financial strain where conventional financing won't work or is difficult to obtain.

The housing market is evolving rapidly. Investors would be wise to understand their options so that they are able to adapt, take advantage of opportunities, and free up liquidity when they need it.

As a company, we only focus on non-resident mortgages for major international real estate investor markets: USA, UK, Canada, Australia, Singapore, Hong Kong, and Thailand.

In the US, our wholly-owned subsidiary, America Mortgages, is the only US mortgage specialist outside the US.

Get in touch with us today to learn more about the structures and options of short-term bridge financing solutions at hello@gmg.asia.

Direct from our Loan Development Team – we have created a solution which allows our international high-net-worth clients to use their liquid asset portfolio to qualify for a U.S. mortgage loan without pledging or encumbrance, nor the requirement of any minimum deposit held at a bank (AUM).

Introducing “GMG U.S. Super-Jumbo+" & "LADMI"

Are you a businessperson with low reported income?

Are you retired with little to no fixed income?

Are you self-employed but with little to no “provable” income?

Are your assets held in a bank with a U.S. branch or presence?

Do you have Trust assets with completely unrestricted use?

If you answered Yes to any of these questions, you will qualify for this program.

Asset Rich, but Cash Poor?

It’s a common issue for high-net-worth investors who report low income but have sizeable asset portfolios including stocks, bonds and other liquid securities.

Traditional banks require pay stubs, employment letters, and credit scores (we have fantastic programs for this as well), but many of our clients are not in the corporate world and require more flexible programs to suit their specific needs.

Separately, private banks will undoubtedly require Assets Under Management (AUM) and normally at least the amount of the mortgage.

We are seeing a trend that high-net-worth investors are now open to looking at financing options outside of their private bank, even if the rate is higher than the subsidised rate they would get from their private bank.

“A small price for freedom,” as one of our European clients recently told us.

Introducing: Liquid Asset Derived Monthly Income “LADMI”

Salient Points:

Qualify for a loan using your liquid asset portfolio instead of income from employment.

No AUM (Assets Under Management) or encumbrance of your portfolio at all, rather, it is ‘only’ to qualify for a loan.

Liquid Asset Derived Monthly Income (LADMI) is calculated by taking total liquid assets and dividing by the duration of most mortgage loans, 360 months (30 years).

LADMI allows you to prove your ability to service the debt without regular income from employment – great for entrepreneurs and high-net-worth investors!

No need to show any other sources of income or employment.

If your LADMI is sufficient to service the mortgage – as well as regular living expenses – you can qualify based solely on this calculation.

No need to cash-in your portfolio or encumber in any manner.

Your assets are used “only to demonstrate” an ability to make the mortgage payments.

Commonly-used Liquid Assets:

Checking or savings accounts

Money market accounts

Certificates of Deposit (CD)

Investment accounts such as stocks, bonds, crypto, and mutual funds

Liquid retirement accounts

[Note] All accounts, banks and or brokerages will be required to have a U.S. presence. IE Fidelity, Capital, Coinbase, Charles Schwab, HSBC etc.

Here is an example:

59-year-old mortgage borrower has:

Cash: $750,000

Investment portfolio: $3,500,000

Cryptocurrency: $300,000

Liquid retirement fund: $500,000

= Total Liquid Assets: $4,300,000 (2+3+4)

This is how we calculate LADMI:

Cash: $750,000

Total Liquid Assets: $4,300,000

Discount Factor: 30%

Discounted Liquid Asset Value: $4,300,000 x 70% = $3,010,000

= Total Allowable Assets: $3,010,000 + $750,000 = $3,760,000

= LADMI = $3,760,000/360 months = $10,444

In this case, we will calculate the borrower’s maximum mortgage payment based on a monthly ‘income’ of $10,444.

The next question you will ask is, what kind of property can this get me?

If we assume a minimum 43% debt to income ratio (DTI) for most lenders and use the current market mortgage rate, you can qualify for a US$1M home (approximately $4,000 P+I monthly payment).

[Note] This is just an example and there are many factors that go into qualifying for a mortgage. This illustration is show that you do not need a salary to qualify for mortgages anymore thanks to our program.

If you have any questions about our GMG U.S. Super-Jumbo+, LADMI or any of our international mortgage or asset-backed financing solutions, please contact us at: hello@gmg.asia or send me a confidential Whatsapp at +65 8499-3229.

Global Mortgage Group Pte. Ltd. is the world's leading international mortgage specialist. Based in Singapore with offices and partnerships across the globe, we connect our international clients to our network of lenders around the world. GMG offers financing solutions in the United States, United Kingdom, France, Canada, Australia and Singapore.

Arabic

Arabic Chinese (Simplified)

Chinese (Simplified) English

English French

French German

German Korean

Korean Portuguese

Portuguese Spanish

Spanish Turkish

Turkish